New Car Sales Statistics UK for Buyers and Dealers (2026)

Learn the numbers behind the UK's new car market, including who's buying, what they're buying and how fast the EV transition is actually moving. Whether you're negotiating a deal or running a forecourt, this is the data you need to make sharper decisions.

Last updated: 12th May, 2026

Anthony Sharkey is COO at New Reg Limited (Car.co.uk, Trader.co.uk, Garage.co.uk), driving innovation in vehicle recycling, logistics, and customer experience.

Listen to this story

The UK new car market is one of the most closely watched economic signals in the country. Registration volumes move in lockstep with consumer confidence, credit conditions and household spending power, so when the numbers shift up or down, they signal something broader before most other indicators have caught up.

Right now, the market is also in mid-transformation. The transition to electric vehicles is reshaping how manufacturers price and stock cars and how buyers think about total cost of ownership. That's not a background trend anymore; it's the central pressure point the entire industry is organised around.

That's why the statistics in this article matter. For buyers, they expose the dynamics that dealers already know but most consumers don't. For dealers, they provide the market-level context for decisions around inventory, EV stocking strategy and where private demand is heading.

Now, let’s dive in.

What's in this article

- 3. Best-selling new car models in the UK

- 4. Which car manufacturers sold the most new cars in the UK in 2025?

- 5. New car sales by region of the UK

- 6. New car price statistics and affordability

- 7. Car finance trends in the UK

- 8. Car depreciation trends in the UK

- 9. CO2 emissions and efficiency statistics for new cars

- 10. Transmission Statistics: Manual vs Automatic Vehicle Sales

- 11. Car ownership trends in the UK

- 12. EV charging infrastructure statistics

- 13. UK car buyer demographics and behaviour

- 14. How have UK new car sales evolved year-over-year?

- 15. Predictions for UK new car sales in 2026

New car sales market statistics in the UK

The UK new car market hit two million registrations in 2025 for the first time since before the pandemic, which is solid progress but still well short of the 2.6 million peak that it hit in 2016. Fleet demand is carrying most of the weight, EVs are the headline growth story and both are reshaping how the market functions today.

What the experts say

Steven Jackson OBE

New car sales in the UK: year-by-year (2015-2025)

How many new cars were sold in the UK in 2025?

A total of 2,020,520 new cars were registered in the UK in 2025 – a 3.5% increase on 2024 and the third consecutive year of growth since the market bottomed out during the supply chain chaos of 2021-22.

This also marks the first time the UK new car market has crossed 2 million new registrations since 2019.

That said, the 2025 figure still sits 12.6% below pre-pandemic levels, and the recovery has been more fleet-driven than consumer-driven. Private buyers made up just 38.6% of registrations.

The UK’s new Zero Emission Vehicle (ZEV) mandate, which requires automakers to sell an increasing percentage of EVs each year, is also inflating volumes somewhat, as manufacturers push EV sales hard to avoid compliance penalties. So the headline number is real progress, but it's not quite the organic demand story it might look like.

How many new cars have been sold in the UK so far in 2026?

Around 234,227 new cars were registered in the UK across January and February 2026, up 4.8% year-on-year and the strongest start to a year since January 2020.

- January alone saw 144,127 registrations, with private sales up 4.5% to 52,397 units and fleet demand edging up 1.6% to 88,269.

- February continued the momentum with a 7.2% year-on-year rise to 90,100 units.

However, geopolitical uncertainty – particularly around U.S. tariff policy and the current conflict in the Middle East – is a potential headwind for the months ahead. Early 2026 looks solid, but it's too soon for us to call it a trend.

How many new cars were registered in the UK in 2025?

The total number of new car registrations in the UK in 2025 was 2,020,520. This is the figure the industry uses as its primary sales benchmark because it represents each vehicle that’s officially recorded with the DVLA for the first time.

New car sales by channel: fleet vs private vs business registrations

The headline number only tells part of the story. To understand what the market’s actually doing, you need to look at who's buying.

- Private registrations made up just 38.6% of all registrations, or 779,587 units total.

- Fleet and business registrations accounted for the remaining 61.4% at 1,240,933 units.

- Fleet registrations accounted for 59.1% of the remaining share (1,194,545 units) and business registrations accounted for the other 2.3% (46,388 units).

- Business registrations saw the highest percentage growth, with sales rising by

- 8.8%.

So while the overall market hit a six-year high, private registrations still sit below 2020 levels.

What that tells us is buyers are still being squeezed by rising car prices and broader cost-of-living pressure. The fleet side recovered faster because corporates have more insulation from those pressures and are also being pushed by emissions policy to cycle through EVs on a schedule.

The market is healthy on paper. For private buyers, it's a harder picture.

Best-selling new car models in the UK

The Ford Puma topped the UK sales charts for the third year running in 2025, with 55,488 registrations. Behind them came the Kia Sportage in second (47,788 units) and the Nissan Qashqai in third (41,141 units).

SUVs occupied seven of the top 10 spaces, which reflects the buyer preference shift we’ve seen building for years. The SUV segment accounted for all three of the top positions. And SUVs have seen a sales volume increase of 117.9% from 2014 to 2024.

In that same time:

- MPVs (Multi-Purpose Vehicles) are down 53.6%.

- Compact cars (e.g. VW Golf, Ford Focus) are down 19.5%.

- Large family cars (e.g. Vauxhall Insignia) are down 47.6%.

- Specialist sports cars are down 60.8%.

- Estate cars and luxury saloons are down 78.5% and 68.7% respectively.

- Supermini registrations fell by 39.3% but remain the most common type of car on UK roads, with 11.9 million in use.

The Vauxhall Corsa and the Volkswagen Golf were the only two that held their ground against the SUV tide, and the Volkswagen Tiguan made history by entering the top 10 for the first time ever. And the Chinese-produced MG HS retained its eighth-place spot, further proof that value-focused brands are becoming a permanent fixture in the mainstream market.

Top 10 best-selling new cars in the UK (2025)

Which new petrol and diesel cars are the most sold in the UK?

The Ford Puma, Kia Sportage, Nissan Qashqai are the three most sold petrol and diesel cars in the UK, with each deriving the bulk of its sales from petrol and mild hybrid-petrol variants. The Vauxhall Corsa, which was the best-seller under £20,000, came in fourth place.

Despite the UK government’s EV push, petrol and diesel retained a slim majority in 2025, accounting for 51.5% of total new registrations. That majority is shrinking – it’s down by 8% compared to 2024 – but it tells you that for most private buyers, the economics of going fully electric still don't stack up, whether that's purchase price, charging access, concerns regarding EVs’ range or simply personal preference.

Also worth noting: Diesel availability is limited across most of these models; the Qashqai and Tiguan still offer diesel options, but they're increasingly niche choices as automakers wind down ICE investment ahead of the 2030 petrol and diesel ban.

What are the best-selling new electric cars in the UK?

The best-selling new electric cars in the UK are as follows:

- Tesla Model Y

- Tesla Model 3

- Audi Q4 e-tron

- Audi Q6 e-tron

- Ford Explorer

Tesla has dominated the UK's battery electric vehicle (BEV) market for years, but 2025 showed that that dominance is under real pressure. The Model Y held onto the top spot with 24,298 registrations, but that's down from 32,872 in 2024 (a 26% drop) and the model slipped out of the overall top 10 for the first time.

Legacy manufacturers like Audi are closing the gap, and Chinese brands are filling in the major gap on the lower end, for budget-conscious drivers who can’t shell out £40,000+ for a new Tesla. In January 2026, the BYD SEAL U entered the overall top 10 new cars at number six, which would have been unthinkable two years ago.

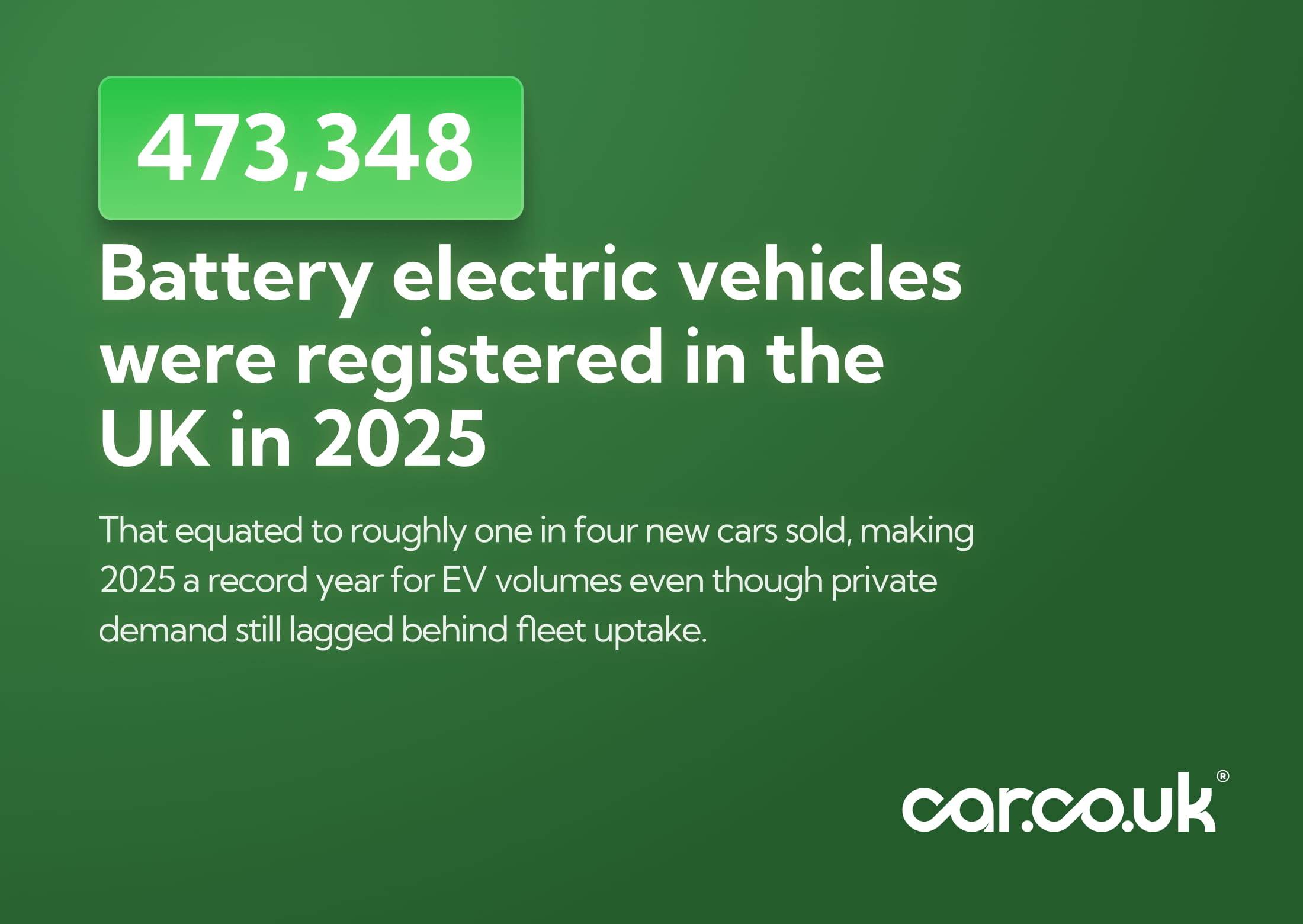

How many new electric cars were sold in the UK in 2025?

473,348 new battery electric vehicles were registered in the UK in 2025, which is a 19.6% increase on 2024 and equivalent to roughly one in every four new cars sold. It's a record volume, and the trajectory is clearly upward.

The caveat worth adding: 23.4% of total new vehicle sales still fell short of the government's 28% ZEV mandate target for 2025, which means manufacturers collectively missed the threshold and therefore faced compliance pressure.

Also, 82% of all new zero-emission cars were registered to company keepers. So the vast majority of the ‘473,348’ figure was driven by manufacturer incentives and aggressive fleet EV pushes specifically designed to avoid penalties. So while the number is genuinely strong, it does not reflect organic consumer demand.

Which car manufacturers sold the most new cars in the UK in 2025?

Volkswagen topped the UK new car market for the fifth consecutive year in 2025, registering 178,607 vehicles and an 8.84% market share. BMW came in second with 122,723 sales, cementing its position as the UK's most popular premium brand. Ford was close behind in third on 118,998 registrations.

Top 5 best-selling car brands (UK, 2025)

Which car brands are the fastest growing and fastest falling?

As far as which brands are the fastest growing, Chinese brands were the story of the year.

- BYD's UK sales surged to 51,422 units (a 485% increase!).

- Newcomer Jaecoo went from near-invisibility to 28,232 registrations.

- Combined sales of Chery-owned Omoda and Jaecoo reached ~54,000, a 13x increase.

- MG, the longest-established Chinese-owned brand, finished the year 10th with 85,155 registrations.

- BYD is now the UK’s 6th best-selling brand, surpassing Tesla for the first time in history.

- Chinese automakers as a whole now account for 9.7% of the new car market.

The toughest year belonged to Jaguar, whose sales dropped 89.6% as the brand pauses combustion engine sales ahead of its repositioning as an all-electric luxury marque. Mercedes-Benz and Audi also struggled, falling 13.1% and 9.2% respectively.

New car sales by region of the UK

New car sales are very unevenly distributed across the UK. Where you live has a significant bearing on how likely you are to buy a new car, and increasingly, how ready your area is for the broader shift to electric.

Which UK region buys the most new cars?

DVLA numbers show that South East England dominated new car registrations in 2024, accounting for 448,800 vehicles, or 22.4% of the entire UK market. The North West came second with 238,500 registrations (11.9%), and London recorded 137,200, representing 6.9% of the market.

While London is the UK's most populous city, there are also significantly higher rates of public transport usage. The cost of running a car is much higher, particularly in the city centre’s Ultra-Low Emissions Zone (ULEZ). These factors reflect in the lower numbers of vehicle purchases.

New car sales in England, Scotland, Wales and Northern Ireland

England accounts for the vast majority of UK registrations by some distance. Scotland was the next largest market with 169,300 registrations in 2024 (8.5% of the UK total), followed by Wales with 68,700 (3.4%). Northern Ireland recorded the fewest new car registrations of any UK nation at 49,800, representing 2.5% of the total market.

New car price statistics and affordability

New cars have never been more expensive, and affordability is now one of the most significant barriers to market recovery (hence why the private market hasn’t rebounded quite yet).

Rising sticker prices, higher interest rates on finance and the premium still attached to electric vehicles have all contributed to a market where fleet and salary sacrifice registrations are picking up the slack that consumer demand can't.

What is the average price of a new car in the UK?

The average price paid for a car in the UK during 2025 was £19,703, but that figure masks significant variation by age and location.

- Younger drivers (18-34) spent the most, averaging over £24,000. This likely reflects the growing role of salary sacrifice and EV leasing schemes, where tax advantages allow younger buyers to access more expensive cars through employer arrangements.

- Drivers aged 55-64 spent the least at £15,449. It’s not that they can't afford more, but that this group is more likely to buy used, hold onto existing cars longer or simply opt for cheaper models. It tracks directly with the ageing fleet data.

- Londoners averaged £28,340, the highest of any region. This reflects the higher incomes and concentration of premium brands which are characteristic of the city, plus the logic of EV ownership with better charging infrastructure.

New car prices by segment

Entry-level pricing varies widely depending on the type of car. Based on the giving buyers a rough sense of what different segments actually cost in 2025:

- City/supermini: The Vauxhall Corsa started at £15,650, making it one of the most accessible new car options on the market.

- Small SUV: The UK's best-selling car, the Ford Puma, started at £25,790.

- Mid-size SUV: The Nissan Qashqai came in at £24,000.

- Premium SUV: The Volvo XC40 started at £35,310.

The jump from supermini to small SUV is the greatest. Buyers are paying a significant premium for the body style alone, which goes some way to explaining why affordability pressure hits hardest in the segments where volume sales should theoretically be strongest.

New car price inflation since 2020

New car prices have risen 25% since 2020 according to official CPI figures, though some industry estimates put the real increase closer to 30-40% once you account for spec changes and model repositioning.

Either way, a car that cost £20,000 in 2020 likely costs somewhere between £25,000 and £28,000 today. Although wages have increased by nearly 30% in that time, adjusting for inflation reveals just a 0.6% increase. That’s why private buyer demand has been so sluggish despite the market recovery.

New car discounts and deals: where buyers are saving

There is some relief emerging. As supply has normalised and competition increased, the average discount on a new car was approaching £6,000 in early 2026 across petrol, diesel and electric models. To put it another way, today’s buyers are effectively clawing back a chunk of the post-pandemic price inflation for buyers willing to negotiate or time their purchase carefully.

Best price given for your car in 30 seconds

Car finance trends in the UK

Most private buyers – particularly those aged 17-24 – finance their new car rather than paying cash. In fact, the UK car finance market was valued at an estimated £39 billion in 2024, highlighting just how central finance has become to new car purchases.

The market runs primarily on three products: Personal Contract Purchase (PCP), where buyers pay a deposit and monthly payments before choosing to hand the car back, buy it outright or part-exchange at the end of the term; Hire Purchase (HP), where the buyer owns the car once all payments are completed; and personal loans, which are fixed amounts you borrow from a bank or lender.

PCP dominates the market, but the mix is shifting.

How many new cars are bought on finance?

In 2025, FLA members' finance supported over 85% of private new car registrations, which makes it the default route into a new car for the overwhelming majority of buyers.

And consumer new car finance volumes grew 7% in the first 11 months of 2025 compared to the same period in 2024, which tells us the appetite is holding up despite affordability pressures.

PCPs, HPs and personal loans: What are the most popular finance products?

PCP is the dominant product in the UK, used by more than half (55%) of new car buyers who finance their vehicle. It works for buyers who want lower monthly payments and flexibility at the end of the term, and it works for manufacturers who want customers to cycle into a new model every 3-4 years.

Hire Purchase (HP) is more of a preference for used cars, and a 2025 survey found that just 8% of those who didn’t pay cash used a personal loan.

Salary sacrifice and EV leasing trends

Salary sacrifice schemes let employees access a new, fully insured and maintained electric car through their employer, with payments taken from gross salary. In this arrangement, both employer and employee save on National Insurance, and employees benefit from significantly reduced income tax. It's one of the most tax-efficient ways to get into a new EV.

The BVRLA reported that salary sacrifice was the fastest-growing car finance method in 2023, with the fleet size growing 41.3% year-on-year.

The tax incentive is the clear driver here: nearly 100% of salary sacrifice cars are BEVs, which reflects the highly favourable Benefit-in-Kind rates that make electric the only sensible choice within the scheme.

Average monthly car finance payments in the UK

Four main variables determine the monthly payments on a new car finance deal: the total price of the car, the size of the deposit, the length of the term and the interest rate (which is directly influenced by the Bank of England base rate).

The base rate rose from 0.1% in December 2021 to a peak of 5.25% by August 2023 in response to high inflation. Then a gradual cutting cycle began in 2024. The current base rate stands at 3.75% as of early 2026.

Car depreciation trends in the UK

Depreciation is the single biggest cost of owning a new car. It’s bigger than fuel, insurance or servicing for most drivers. The moment a new car leaves the forecourt it starts losing value, making car depreciation one of the most important factors in the total cost of ownership calculation.

How quickly a car depreciates varies significantly depending on its fuel type, brand and model, but over a typical three-year ownership period that loss can run into tens of thousands of pounds.

Which cars hold their value the best?

Premium and sports cars dominate the slowest-depreciating list, with the Lamborghini Urus and the Porsche 718 Cayman GT4 RS being the slowest-depreciating cars after a three-year period. That said, the Dacia Duster is a notable outlier, which just goes to show value-for-money and strong residuals aren't mutually exclusive.

Slowest depreciating cars in the UK (2025)

Depreciation by fuel type: petrol, diesel, hybrid and electric

Fuel type has a significant impact on how well a car holds its value, and the results might surprise some buyers currently weighing up an EV purchase.

Average car depreciation by fuel type (UK, 2025)

Hybrids currently top the table because there’s strong buyer demand for them, and they hit the sweet spot they occupy between conventional and fully electric. Petrol and diesel are close, with diesel's long-term decline in popularity eating into its residuals slightly.

Electric is the most complicated story. Some premium EVs like Tesla are among the fastest depreciating cars on the market, losing around 45% of their value in three years, but certain other EV models buck that trend.

Rapid model updates, falling new car prices from Chinese competitors and lingering buyer uncertainty about battery longevity are all weighing on EV residuals in ways that are proving hard for us to predict.

Fastest depreciating cars in the UK (2025)

While the slowest depreciating cars in the UK are mainly sports cars (the Lamborghini Urus takes the number-one spot), the fastest depreciating ones are EVs and luxury saloons.

There are tons of reasons why EVs lose their value so quickly. Increasing supply and choice, falling new prices, and manufacturer discounting to meet ZEV mandate targets all driving values down.

The Jaguar I-Pace is a particularly stark case. I-Pace owners collectively saw an estimated £432 million wiped from their vehicles' value over three years.

CO2 emissions and efficiency statistics for new cars

CO2 emissions from new cars matter for two reasons: environmental targets and what drivers actually pay in tax. Vehicle Excise Duty (VED) is directly tied to a car's emissions and car tax bands at the point of registration, meaning cleaner cars cost less to tax, and zero-emission vehicles are currently exempt entirely. The shift toward electrified vehicles is accelerating progress on both fronts faster than most forecasts predicted.

Average CO2 emissions of new cars in the UK

The average CO2 emissions for a new car sold in 2025 fell 10.1% to 91.8 g/km, following a 6.2% reduction in 2024 when the average stood at 102.1 g/km. Two consecutive years of meaningful cuts reflect the growing share of EVs and hybrids in the sales mix, and suggest the market is finally moving fast enough to matter environmentally, not just on paper.

CO2 emissions trends over time

Since 2008, average new car CO2 emissions in the UK have dropped 24%, from 169.5 g/km to 129.4 g/km by 2024, with 2025's figure of 91.8 g/km representing a significant further step.

The EU set a 95 g/km target for new car emissions (a threshold which SMMT reports that the UK market has now effectively breached ahead of schedule), driven almost entirely by the rising volume of battery electric and plug-in hybrid registrations.

VED (Vehicle Excise Duty) tax band distribution

VED is calculated based on a car's CO2 emissions at first registration, meaning the tax landscape for new car buyers is shifting right alongside the emissions data.

The trend today is that average emissions are falling. As more buyers move into lower bands or full exemption, the long-term implications for VED revenue are significant enough that the government has already made changes to how EVs are taxed from April 2025 onwards.

Now:

- First-year (showroom tax) bands for cars registered after 2025 range from £10 for ZEVs to £5,490 for those polluting more than 255 g/km of CO2.

- From the second year onward, they pay a flat £200/year standard rate regardless of emissions, plus £425/year expensive car supplement if the original list price exceeded £40,000 (£50,000 for EVs from April 2026).

Transmission Statistics: Manual vs Automatic Vehicle Sales

There’s been a huge shift away from manual gearboxes in the past few years for two reasons: consumer preference and the fact that all electric vehicles are automatic (since they don’t have a gearbox).

How many new cars are sold with automatic gearboxes?

In 2024, 78% of new cars sold in the UK had automatic transmissions. And in 2025, there were 404 automatic-only models available, compared to just 96 manual-only. So there were about four times as many automatic models available as manuals.

The decline of the manual gearbox

The market share of manuals has diminished to just 22% of new cars sold. There are three factors driving this:

- Driver habits and preferences

- Availability, particularly with EVs

- Market shifts making automatic the default

- General fuel usage and costs

While manuals still accounted for 70% of the cars on UK roads back in 2022 (and thus likely still make up the majority), the reason for that is the average age of cars on the road skews old. When we’re talking about new cars sold, that isn’t the case at all.

Car ownership trends in the UK

The UK "car parc" (the collective term for all registered vehicles currently in use) has reached an unprecedented scale. At the same time, it’s also the oldest on record. The ageing profile creates a massive replacement cycle opportunity for the new car market as owners eventually look to modernise.

How many cars are on the UK roads?

As of the end of 2024, there were 41.7 million licensed vehicles on UK roads, of which 33,967,000 were cars. The SMMT's Motorparc data, which captures a broader picture including SORN vehicles, puts the total number of cars in use slightly higher at 36.2 million.

Average age of cars on UK roads

Age matters too. And people are holding onto their cars longer than ever.

- At the end of 2024, licensed cars were 10 years old on average (the oldest on record).

- Average age has increased by 16% since 2019, when the average age was just 8 years.

- 31% of cars on UK roads in 2024 were more than 12 years old.

That last point is the most interesting. If nearly a third of cars on UK roads predate 2012, that means a significant portion of the fleet is older than current safety and emissions standards. In other words, even as new car sales recover and EV adoption grows, the actual cars British people are driving day-to-day are getting older and more polluting.

UK car ownership by household

Nearly half (45%) of UK households own one car, and just over one-third (34%) own two or more vehicles. This means that only 22% (nearly 1 in 4) UK households do not own a car.

Geography plays a big role in this, and we can see this within the Greater London area. According to recent data from Transport for London:

- 62% of households in inner London were car-free in 2023/24.

- Only 33% in outer London were car-free during that same period.

- Outside London, just 18.3% of households don't have a car.

Of course, income plays a role as well. According to the government’s 2024 National Travel Survey, 40% of households in the lowest income quintile didn’t have access to one, while just 14% in the highest had the same problem.

EV charging infrastructure statistics

Public charging infrastructure is arguably the single biggest lever for EV adoption in the UK, more than purchase price, more than range. The network has certainly grown rapidly, but coverage is deeply uneven, with London and major urban centres significantly better served than rural areas. For thousands of potential buyers, the question isn't whether they want an EV; it's whether the infrastructure where they live makes one viable.

How many public EV chargers are there in the UK?

As of October 2025, the Department for Transport reported there were 86,021 public EV charging devices across the UK, of which around 20% (17,356 units) were rapid or ultra-rapid chargers capable of 50kW or above.

The ‘20% rapid charger’ figure is the one we want to scrutinise. It means the majority of the network is still slow AC charging, which is fine for overnight charges and top-ups but largely useless for en-route charging on longer journeys.

Our prediction: Until rapid and ultra-rapid chargers comprise a much larger share of the total, range anxiety for drivers without home charging isn't going away, and that cohort skews heavily toward renters, flat-dwellers and lower-income buyers the government most needs to convert.

EV charger growth rate

The Department for Transport also reported that the UK added 14,316 new chargers in 2025. That’s a 19.5% increase in network size in a single year, and it sounds impressive until you put it next to EV sales growth.

The SMMT has explicitly flagged that installation pace isn't keeping up with sales, and the maths backs that up:

- BEV registrations grew 19.6% in 2025.

- The charger network grew 19.5%.

They're moving in near-lockstep, which means the ratio of cars to chargers isn't improving; it's just holding steady at a level that's already insufficient. For the network to actually get ahead of demand, charger growth needs to meaningfully outpace EV sales growth for several consecutive years. That's not happening yet.

EV charger to car ratio by region (2022-2024)

Charging infrastructure readiness varies dramatically across the UK, and the gap matters because it's one of the most cited reasons private buyers hold off on EVs.

Being a city that’s 15 times more densely populated than the rest of the UK, but with lower per-capita vehicle ownership, London leads with 11 plug-in cars per public charger.

But the regional differences are stark. The North West, South East and Northern Ireland are sitting at 50:1+, meaning over 50 plug-in cars competing for every single public charger.

UK car buyer demographics and behaviour

In the UK, the new car buyer is older and more price-driven than the market narrative often suggests. Private buyers skew toward the 55+ age group, and prioritise price and reliability over everything else. And while they’re predominantly buying from physical dealerships, they’ll travel an average of 45 miles to do it.

Age and gender profiles of UK new car buyers

YouGov studied car buying preferences across Britain, and what they found was interesting:

- The typical UK new car buyer skews older and wealthier. Buyers aged 55 and older are the most likely to purchase new, while younger buyers aged 18-24 heavily favour used cars, with 57% intending to buy second-hand versus just 35% opting for new.

- Men are significantly more likely to buy new. 34% intend to purchase new in the next 12 months, versus just 27% of women. Women lean used, with 55% planning to buy second-hand compared to 49% of men.

- Low- and high-income buyers show a higher preference for used cars. Nearly 58% of low-income buyers chose to go second-hand. Interestingly, even high-income buyers earning over 200% of the median still favour used (45%) over new (36%).

- There’s loyalty to both sides. 67% of buyers who currently own a new car intend to buy new again, while 65% of used car owners plan to stick with used — suggesting purchase behaviour is heavily path-dependent.

Out of those who did buy new, it revealed that younger drivers (18-34) spent the most on cars in 2025, with an average spend of more than £24,000. Meanwhile, drivers aged 55-64 spent the least, with an average of just £15,449.

What do UK car buyers prioritise when buying a new car?

Price is the single most important factor for UK new car buyers, with 52% citing it as their top priority. This is a figure we only see growing as cost-of-living pressure continues to squeeze household budgets like it has over the last few years.

Reliability (41%) and practicality (33%) round out the top three, which paints a pretty clear picture: most buyers want a car that's affordable to buy, won't break down and fits their lifestyle and needs. Not particularly glamorous, but honest.

The stat worth flagging for dealers and manufacturers is the eco-friendliness number. Only 7% of buyers ranked it as a top factor, which creates a real tension with the direction government policy is pushing the market.

Manufacturers are under mandate to sell more EVs, but the majority of buyers aren't walking into showrooms caring about emissions. They're motivated by value.

That gap between policy intent and consumer priority is arguably the central challenge facing the UK car market right now, and it explains why EV adoption is being pushed through fleet channels and financial incentives rather than organic private demand.

Where do UK buyers purchase their new cars?

According to 2025 Car Buyer’s Report, dealerships are still the dominant purchase channel for new car buyers, with 49% of them choosing a dealer for their most recent car purchase. Independent dealers took 29% of purchases, and online marketplaces accounted for just 7% despite years of hype around digital retail in automotive.

What’s interesting is that the average UK driver travelled 45 miles to purchase their car in 2025. If people are willing to drive almost an hour each way to find the right car at the right price, it’s safe to say there’s no loyalty to the nearest forecourt.

If you’re a dealer, that’s both a threat and an opportunity: you're competing with showrooms well outside your immediate catchment, but you can also pull buyers from much further afield if your stock, pricing, reputation and marketing are strong enough.

How have UK new car sales evolved year-over-year?

Over the past two decades, UK new car sales have been repeatedly bent out of shape by financial crises, political uncertainty, a global pandemic and finally by an accelerating shift in what kind of car buyers need. Understanding where the market sits today means tracing those disruptions back to their roots.

The table below summarises annual registrations from 2008 to 2025:

New car registrations in the UK (2008-2025)

Let’s look at these changes more in detail now.

The financial crisis and scrappage era (2008-2012)

The 2008 financial crisis sent sales into freefall, with monthly declines of 20-30%. The government's 2009 scrappage scheme (£2,000 off a new car when scrapping a car that was 10-years-old) artificially propped up demand, accounting for roughly a fifth of all registrations that year. Once it ended, the market softened again before recovering in 2012.

The boom years and Dieselgate (2013-2016)

Cheap finance and rising consumer confidence drove four consecutive years of strong growth, peaking at 2,692,786 registrations in 2016. But two things cracked that foundation: the Brexit referendum in June 2016 introduced economic uncertainty, and Volkswagen's Dieselgate scandal, which broke in 2015 and totally ruined buyer sentiment toward diesel.

The long slide and COVID collapse (2017-2021)

Sales fell every year from 2016 through to 2020. Brexit paralysis, the diesel collapse and a 2018 emissions testing shake-up all eroded confidence. Then COVID-19 delivered the worst year in decades: a 29.4% crash to 1.63 million units. Then, the expected 2021 rebound was throttled by the global semiconductor shortage, which left supply well short of demand.

The recovery (2022-2025)

Supply chains normalised, triggering a 17.9% rebound in 2023 and steady growth following in 2024 and 2025. The market crossed 2 million units for the first time since 2019 last year but remains roughly 330,000 units below the 2016 peak, with private buyer demand still soft and EV adoption lagging government targets.

Predictions for UK new car sales in 2026

The UK automotive sector generated £92 billion in turnover in 2024, contributing £25 billion to the economy and supporting nearly one million jobs across manufacturing, supply, retail and servicing.

It's also heavily trade-dependent; the UK exports 77% of the cars it builds, with total car export value reaching £28 billion. That makes it one of the industries most sensitive to geopolitical shifts like the US tariffs the United States President introduced in 2025.

UK new car market forecast for 2026

The SMMT forecasts 1.4% growth in 2026, which would bring the market to 2.048 million units. Modest but steady, and we’d say it’s fairly reasonable given where private demand is sitting. The fleet market will keep doing the heavy lifting.

Electric vehicle forecast for 2026 and beyond

BEVs are forecast to hit 28.5% market share in 2026. That's meaningful progress, but it's largely being driven by fleet buyers and manufacturer incentives rather than organic private demand. In other words, the number is somewhat fragile.

Since manufacturers are expected to just barely clear the bar, we expect them to do so through a mix of aggressive pricing, manufacturer subsidies and strategically timing registrations toward December (which is what happened in 2024 and 2025).

ZEV mandate targets and timeline

The ZEV mandate requires 28% zero-emission sales per manufacturer in 2026, rising incrementally to 80% by 2030 and 100% by 2035. Like we mentioned above, SMMT insights show that manufacturers are on track to just clear the 2026 bar.

But the trajectory toward 80% by 2030 is steep. With private buyers still hesitant (if not financially constrained) and charging infrastructure patchy outside major cities, hitting those later targets without significant policy intervention still – to us – seems overly ambitious.

About Car.co.uk

Share on

Latest news & blogs