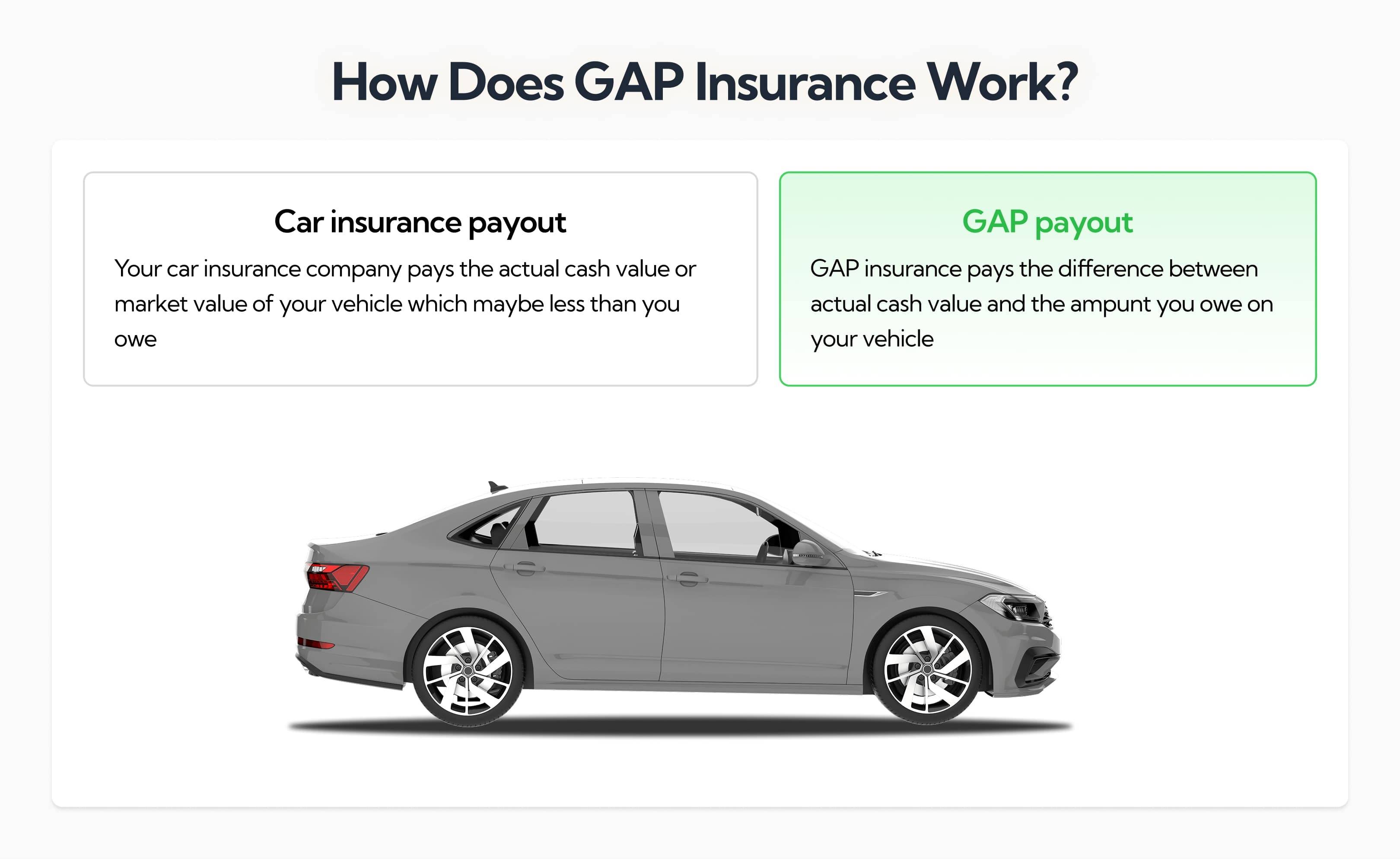

How Does GAP Insurance Work?

GAP insurance covers the shortfall between your car insurer’s payout and either the car’s original price or what you still owe on finance if it’s written off or stolen. With cars losing value quickly, it protects you from unexpected costs that your standard policy won’t fully cover. In this guide, I'll explain the ins and outs of how it works.

Last updated: 3rd October, 2025

Award-winning CEO driving growth and social impact across automotive, recycling, and technology-led enterprise platforms.

Listen to this story

Cars lose value quickly. The moment you drive one off the forecourt, it's worth 20% less. And by the time it's three years old and ready for its first MOT, it's tanked by 50% or more.

If your car is stolen or written off in an accident, your standard insurance usually pays only its current market value, which will be thousands less than what you paid or still owe on finance.

That’s where GAP insurance (Guaranteed Asset Protection) comes in. It’s an optional add-on policy that covers the difference between your insurer’s payout and either the car’s original purchase price or the remaining balance on your loan or lease.

In this guide, I'll explain exactly how GAP insurance works, the different types available and when it makes sense to add it to your cover so you can protect yourself from unexpected financial losses.

What's in this article

Guaranteed Asset Protection or ‘gap’ car insurance is a type of policy designed to be used in conjunction with your standard car insurance. Gap insurance was first conceived to cover the potential financial losses of car owners if their vehicle experiences certain unfortunate circumstances. For example, if a car is so badly damaged in a road accident that it can’t be repaired and must be written off, or if you are a victim of theft and your car is stolen, a gap insurance policy can assist the owner in reclaiming the full financial investment they made when they first purchased it.

But exactly how does gap insurance work? If your car has been totalled and must be destroyed or is stolen, your standard car insurance - compulsory to car owners by law here in the UK - will only give you a payment for the amount your vehicle is valued at when you make a claim. If you bought your brand new car three years before an incident took place, it’ll typically be worth around 60 percent less than the price you paid originally due to the rapid rate of depreciation on new cars. This means that depending on what you paid for your new car, on average you’ll be losing over half of the car’s original worth when you receive your payout from the insurance company.

At this point you can either buy a car of equal value to the one written off or make up the difference yourself and put it towards buying yourself an all-new replacement vehicle. That is, unless you have purchased a gap car insurance policy. This additional insurance acts to cover the difference or ‘gap’ between what your car insurance provider will pay out and what the original value of your vehicle was when you purchased it. Return to Invoice or RTI car insurance is an example of one form of gap car insurance available. It considers your original invoice price when you purchased a car and pays out the difference between this and the amount your car insurer will cover you for, ensuring you don’t suffer a financial loss.

If you’re curious about how gap car insurance works and how it might help you out in a number of circumstances such as theft, a crash or if you purchased your car using a finance deal, then read on for all the answers you’re after.

How does gap insurance work after a car is stolen?

If your car has been stolen, gap car insurance can help cover the cost. When a vehicle is the object of a theft and you report it to your car insurer, they’ll assess the vehicle for its worth and pay out what its current market value is at the time of your claim.

If you’ve got gap car insurance, it will cover the ‘gap’ between your insurance company’s payout, known as either the ‘total loss’ or ‘maximum’ payment, and the amount you paid for it originally, or its value at the time of purchase depending on the type of gap cover you possess.

As with any form of car insurance, the theft of your vehicle must not be your own fault to receive a payment. If your home was burgled and your car keys were taken, for example, then this would be considered outside of your area of control and you’d be covered. However, if you left your vehicle unlocked with the keys remaining in the ignition, the theft would be attributed to your negligence and it is unlikely that you would receive a payout from your gap insurer.

How does gap insurance work after a car is totalled?

After your car has been in a collision, and if it’s crashed totalling it beyond repair, gap insurance is designed to assist you. Normally sold at the time of buying from a dealership, it’s a kind of insurance more commonly sold to new car buyers. While second hand car buyers can also sometimes have the option of purchasing gap car insurance, the vehicle they’re taking it out on must be less than seven years old for insurers to offer it.

As with theft, if your car has been written off, your standard car insurance policy will offer you a settlement based on their assessment of your car’s current market value. New cars lose their worth at an alarming rate, with a 40 percent drop in the first year considered average, and after three years this is typically closer to 60 percent. Gap car insurance has been developed to cover this fall in value and cover the ‘gap’ between what your insurer will pay and how much you originally bought your car for, or its value at the time.

As your car insurer will only pay you for what your car is currently worth, you can either stump up the extra cash to buy yourself a new car or buy one that is like-for-like with the model that was totalled.

Gap insurance however, will allow you to purchase a brand-new car if your vehicle is written off.

What the experts say

Anthony Sharkey

How to use gap insurance

As previously mentioned, gap car insurance works side by side with your standard car insurance policy and fills the gap between what a policy will pay out and the original purchase price of a car.

Gap car insurance can be useful if you’ve bought your new vehicle using a finance agreement, like a personal loan or personal contract plan (PCP). If your car, purchased with finance, must be written off or is stolen, then due to the interest on a loan combined with the depreciation of your vehicle your car insurance policy won’t actually cover the full amount of your debt.

If this happens, you’ll either need to come up with the money to pay off the existing finance or keep making your monthly repayments on a car that was stolen or has been scrapped.

There are types of gap car insurance specifically designed to be purchased alongside cars bought with finance. With this kind of gap insurance, you’ll be covered for the difference between what your insurance provider will pay out and how much your outstanding finance is due on the car, allowing you to settle your debt.

If your finance deal is taken out over a term of many years or has a high interest rate, you can use gap car insurance to cover yourself. If your finance agreement is a personal contract plan, it could be especially worthwhile to take out gap insurance cover. PCPs have a final one-off large sum to be paid at the end of the agreement known as a balloon payment. Without gap car insurance, you’ll be covering this large sum yourself just to settle your debt with nothing to show for it, rather than to own the vehicle outright.

If you think that you’d only be happy with a completely new car if your car had been written off or stolen and had to be replaced, then using gap car insurance can be an option worth considering. This is particularly true if you don’t possess the funds to top up the amount your car insurer is prepared to pay out. The gap insurance will handle this for you and cover the difference between what your car was worth when you bought it, or the price you originally paid, and the car insurer’s payout.

It’s also worth making sure you understand what your car insurance policy covers you for before looking into getting gap insurance. Many new cars come complete with a policy that will offer owners a brand new replacement car if it’s damaged beyond repair and must be written off or stolen in the first, and sometimes second, year of ownership. If you’ve got this kind of cover for your new car then gap car insurance could prove unnecessary.

Other circumstances in which gap car insurance might not be of use to you would be if you can make up the difference in price yourself to purchase a brand new car should something like a theft or a crash happens, or if you don’t require a brand new car and would be satisfied with a like-for-like replacement vehicle.

While gap car insurance is often sold by car dealerships, it’s worth noting that such cover is considerably less expensive if purchased online through brokers and specialty car insurers. While dealerships offer cover for around £300-£375 for three years, online you can find similar gap insurance for between £120 and £150.

Before making a claim on your gap insurance it’s worth checking out your terms and conditions to see if it states any limitations on submitting a claim, what information they might require and what your policy excess is so that you’re fully prepared. It is also considered sound advice to contact your gap insurer before accepting any offered settlements from your car insurer.

Remember that if you’re not satisfied with your car insurer or your gap car insurance provider, you’re entitled to contact the Financial Ombudsman. A term of six months from the point you reach a stalemate with your insurance provider is open to you to contact the Financial Ombudsman Services and register your complaint officially.

About Car.co.uk

Share on

Latest news & blogs